As consumers shift their attitude towards financing, the Buy Now Pay Later sector takes the centre stage. With the emphasis on flexibility, transparency, and seamless digital experiences, the Buy Now Pay Later model is becoming a staple in the modern consumer's financial toolkit, reshaping how we approach and fulfil our purchasing desires.

In this guide, we’ll explore the evolution of Buy Now Pay Later, its advantages against traditional credit, the multiple ways of building BNPL solutions, and how Edenred Payment Solutions can support fintechs to deliver modern financing options.

The growth of Buy Now Pay Later

Buy Now Pay Later (BNPL) is amongst the most modern forms of financing, one that is reshaping how consumers approach their purchasing decisions. As consumers combat the rising cost of living, the adoption of BNPL becomes even more commonplace, as it frees up consumers from the immediate financial commitment associated with traditional debit card payments.

Fuelled by the digital transformation of financial services, and socio-economic factors, the BNPL sector is predicted to grow exponentially – making it a €300 billion industry in Europe by 2025.

The growth of BNPL isn't confined to a specific industry; instead, it has permeated various sectors, from retail to travel and even healthcare. Against a challenging economic backdrop and a hyper-competitive market, merchants have rapidly embraced Buy Now Pay Later solutions.

Following the adoption of BNPL solutions, 47% of merchants have experienced an increase in average order value, while 57% benefitted from an increase in conversions.

For retailers, offering BNPL solutions directly to consumers is challenging due to the complexities around liquidity management. However, tech-savvy fintechs, which focus solely on delivering BNPL solutions, are now providing retailers with a much faster and seamless route to integrate BNPL offerings into their checkout flows.

What is BNPL?

Simply put, BNPL is a form of financing that allows consumers to break down the cost of their purchases into convenient, interest-free instalments, tailored to their needs.

Historically, BNPL has been embraced by the younger demographic, as it aligns with their desire for financial flexibility and transparency.

As more people across generations get accustomed to online shopping, the European e-commerce market revenues are projected to witness a substantial increase, reaching $206.4 billion (34.14%) between 2024 and 2028, further intensifying the demand for flexible payments.

Fintech companies, known for their agility and cutting-edge technology, are seizing the opportunity to capitalise on this expanding market and integrate flexible payment options at checkout.

How does BNPL work?

The journey to using BNPL is incredibly simple from a consumer's standpoint.

Typically, users initiate the process by selecting the Buy Now Pay Later option at the point of sale (POS), either on a merchant's website or app. At this point, they will be directed to the BNPL provider’s platform to create an account, and provide personal details, what is known as “Know Your Customer” (KYC) requirements, for a soft credit check used to approve the lending. Once these initial steps are successfully completed, and the credit limit is approved, consumers can select their preferred payment terms and finalise the purchase.

BNPL providers, like Oney and Pledg, facilitate lending to customers by enabling split payments online, while fintechs, such as Viabill and Klarna, go one step further and issue cards to their users for greater accessibility. In both cases, merchants receive an upfront payment for the purchase amount by the BNPL provider.

Repayments, designed with user convenience in mind, offer flexibility to match individual preferences. Consumers can opt for the hassle-free route of setting up Direct Debit mandates, ensuring timely repayments without the need for manual intervention. Alternatively, users can choose to pay with their own payment cards, best suited to their cash flow needs. In essence, the BNPL process not only simplifies the act of making purchases but also democratises the ability to manage repayments, placing control firmly in the hands of consumers.

.png?width=781&height=291&name=BNPL%20flow%20-%20LATEST%20(1).png)

BNPL vs traditional credit systems

With the rise of Buy Now Pay Later, the battle between modern flexible payments and traditional credit systems has intensified. While both options offer the perk of splitting purchase costs over time, BNPL is a well-liked alternative, with its user-friendly application process, granting consumers quicker access to funds at the point of sale.

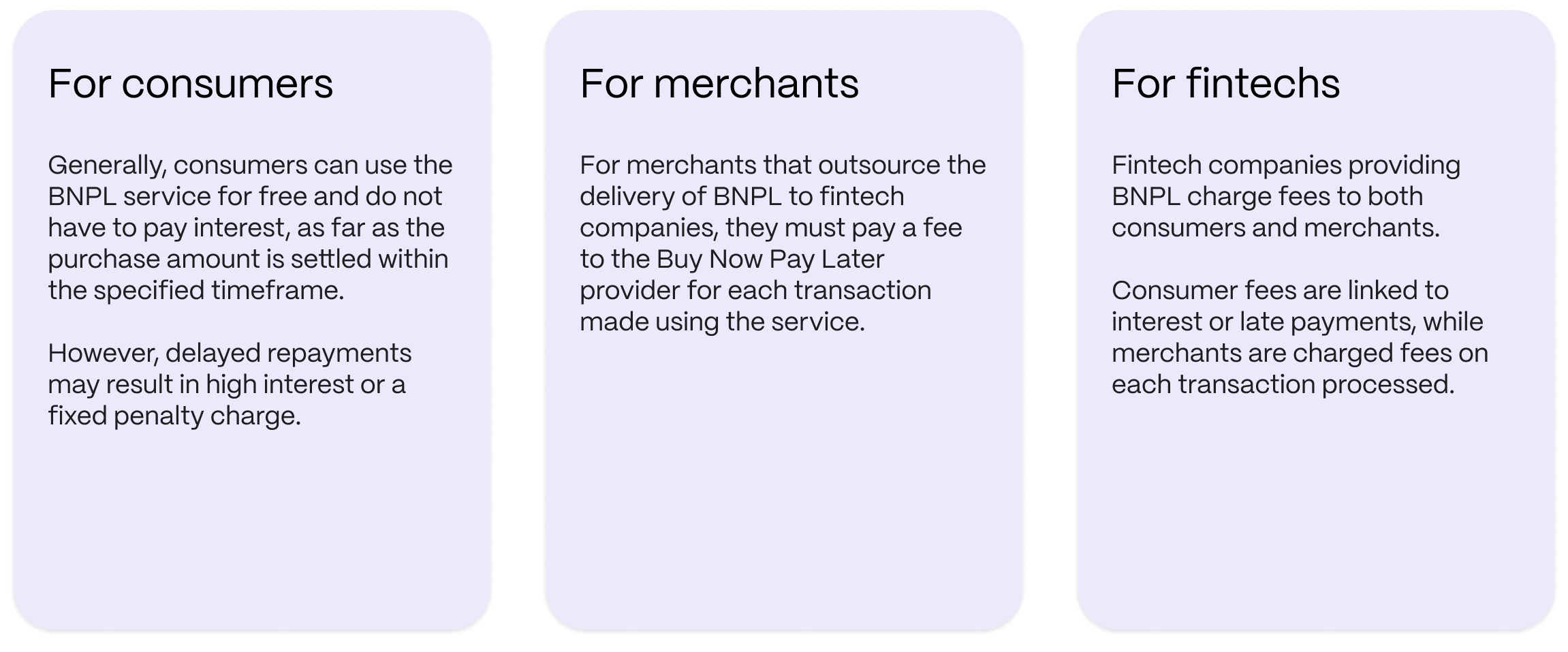

Unlike the endless requirement of paperwork and credit scrutiny of credit card applications, BNPL often skips the hard credit check, simplifying the process for consumers. Additionally, the annual fees and accruing interests that come with traditional credit cards find no home in the BNPL sector.

In summary, BNPL streamlines accessibility to credit options, making it a popular option in the ongoing duel between old-school credit systems and new-age financing.

Benefits of BNPL

Buy Now Pay Later offers consumers a plethora of benefits. One of its prime advantages lies in the flexibility it grants to shoppers, allowing them to easily divide their purchases into convenient, bite-sized repayments, while still enjoying immediate access to their desired products or services. Not only that, but BNPL is a cost-effective option as it doesn’t carry interest fees, provided that repayments are made on time.

This financing model eases the strain on consumers' wallets, but also serves as a more accessible route to financing. Unlike traditional methods, BNPL providers often waive the need for a hard credit check, making it a viable option for those new to credit or grappling with a less-than-ideal credit score.

Understanding BNPL fees and costs

The Buy Now Pay Later model is a convenient option for consumers, merchants, and fintech companies alike, as the fees and costs associated are clear and straightforward.

The importance of regulations for BNPL

With the rapid growth of Buy Now Pay Later services, the importance of regulation has become a focal point, driven by the need to safeguard consumers against potential pitfalls. As the popularity of BNPL rises, so does the concern surrounding late fees and hidden charges that can catch users off guard. The enticement of quick and easy access to credit amplifies the necessity for regulatory measures. The younger generations embracing BNPL may not fully grasp the long-term implications of their spending decisions, making them more susceptible to falling into severe debt.

Regulation in the BNPL market is not about stifling innovation, but rather about ensuring responsible usage. With the ease of obtaining credit, there is a genuine risk that consumers might lose track of their spending, leading to financial strain when repayments become due.

By instating appropriate regulatory frameworks, authorities can guide BNPL providers, with the tools and knowledge they need, to navigate the BNPL landscape responsibly and protect consumers. As the financial industry evolves, thoughtful regulation becomes a crucial ally, fostering a balance between innovation and safeguarding consumers against the risks of unchecked credit accessibility.

How Edenred Payment Solutions can help you deliver Buy Now Pay Later

In a hyper-competitive market, and with both consumers and merchants’ needs forever changing, we have built customisable services and products to help fintech companies offer the most modern and convenient financing solutions. Here’s how we make it happen:

Enabling fintechs to provide access to credit for their users

Overcome tech and regulatory hurdles

Providing access to credit for your users through cards, becomes simple when you work with us. By relying on our card processing technology and licensing support, you can get to market faster bypassing the challenges of obtaining an e-money license from regulatory authorities and building your own tech infrastructure. As the licensed entity, we enable you to open master accounts, either with a UK Account Number and Sort Code or EU IBAN, depending on your needs, to hold and manage the credit funds associated with your BNPL programme.

In simple words, you have total control over your cashflow, while we are in charge of safeguarding the funds, responding to regulators on your behalf, while keeping you compliant at all times.

Build your ideal program with APIs

Through our robust but flexible APIs, you can build your ideal BNPL program. As our APIs integrate seamlessly with any mobile or web app, your users can have access to easy-to-use features, such as viewing card details, checking transaction history, and remaining credit balance, to manage their BNPL account all in one place.

Not only that – our technology enables you to easily manage your card program, like configuring usage, and our APIs allow you to access banking features to manage the master account, such as adding funds, which you can do through Faster Payments and SEPA.

Create a universal card product

As a Mastercard® Principal Member, we offer the full end-to-end issuer managed Mastercard service and BIN sponsorship, including the processing and settlement of all card transactions. With physical and virtual cards linked to the Mastercard® card scheme, we enable you to increase product adoption by creating a universal product that gives your customers the opportunity to spend their credit across a wide range of merchants.

Finally, as a growing number of shoppers increase their usage of mobile payments, we can enable card tokenisation and support for Apple Pay and Google Pay, for checkout in-store and online, so your customers always have the flexibility to access their credit, however they choose to shop.

Since its launch in 2014, ViaBill has been delivering solutions to both merchants and direct to customers throughout Denmark, Spain, and the US. The member service, offered direct to consumers, allows customers to spread the cost of purchases, offering transparent, flexible, and smart payment options.

See how we how we supported the expansion of ViaBill’s BNPL solution through card issuing.

Helping fintechs to manage payments with merchants

Simplify payments to merchants

When providing instalment payment options at ecommerce checkout, we can provide the payment mean for you to pay the merchant upfront via Mastercard virtual cards. As the customer completes their purchase online, a single use virtual card (VCN) is issued and processed instantly for the full amount of the transaction (minus fees), while your customers make repayments to you later in instalments.

Benefit from a quick and simple integration

With our suite of functional APIs you can easily integrate virtual card payments into any backend environment, and manage the virtual card lifecycle by taking actions such as “block card”, “update card details”, and more.

Have full visibility for streamlined reconciliation

To help you stay on top of transactions processed, we enable real-time alerting through customisable webhook notifications, so your platform can capture consumers’ card details as each transaction happens at the point of sale.

To simplify the reconciliation of these transactions, we provide integration reports at your preferred frequency, be it daily, weekly, or monthly, enabling you to seamlessly reconcile with your accounting system.

Build a solution that fits your business needs

Recognising the diverse needs of businesses, we offer a range of virtual cards. You can choose from Debit, Credit, and Prepaid Mastercard cards. This tailored selection allows fintechs to align their choices with the specific requirements of both their operations and merchants. Regardless of the card type you pick, our in-house robust processing engine can handle virtual card transactions at scale, ensuring a consistent experience for users and merchants alike.

In conclusion

The ease with which consumers can access credit through Buy Now Pay Later has catapulted this service into mainstream adoption, especially among younger demographics. As users continue to make the most of the benefits BNPL has to offer, fintech companies play an increasingly pivotal role.

Edenred Payment Solutions has now become the go-to choice for fintech companies seeking a fast-track to deliver Buy Now Pay Later solutions. With robust tech functionalities and licensing, we empower businesses to effortlessly build, expand, and enhance their offerings to quickly respond to consumers and merchants’ needs.

In the years to come, this sector is predicted to grow exponentially, and with an emphasis on regulations and consumers protection, it may well change how flexible payments are delivered and utilised.

Deliver your perfect alternative financing solution

With our robust tech infrastructure, customisable services, and payments expertise, we can provide all the tools fintechs need to seamlessly deliver modern BNPL solutions.